Global Sustainable Bonds with Jessica Zarzycki, Nuveen

Global bond markets are actually larger than global share markets yet they receive far less attention in discussions about sustainable investing.

Increasingly, those bond markets are financing projects such as renewable energy, affordable housing, and community development.

Hi everyone, and welcome to Your Money Matters, with me, Dr Rodger Spiller, exploring how investing can help you make money and make a difference.

However, you're experiencing this - whether audio or video - we're glad you're here.

As a specialist ethical investment adviser through my advisory firm, Money Matters, I aim to educate individuals about how they can make money and make a difference.

This podcast is purely educational - it’s not financial advice.

Everything we cover today is for information and education purposes only.

Introducing the Topic

In today's podcast, we're exploring a corner of the investment world that many New Zealanders may not have considered — investing for impact in global sustainable bonds.

My guest in the studio is Jessica Zarzycki, a Portfolio Manager at Nuveen, one of the world's largest investment managers.

This podcast provides a special opportunity to go deeper into this important subject.

We’ll explore questions such as:

When it comes to international fixed interest, can investors aim for both strong financial outcomes and positive impact?

And:

How can a genuine impact bond be distinguished — given concerns that some investments may overstate their environmental or social benefits?

Understanding Bonds (Fixed Interest Explained)

Before I introduce Jess and the fund she co-manages, I’ll take a couple of minutes to provide some context about bonds, as not everyone tuning in may be familiar with these concepts.

Bonds are classified in Money Matters client plans and portfolios as fixed interest investments.

In a diversified portfolio, fixed interest is generally regarded as a defensive investment.

An example of fixed interest most people can relate to is bank term deposits, and for greater risk - and therefore higher expected return - finance company deposits.

However, there are many other options.

These include:

government bonds, where you are lending to the government…

semi-government bonds, such as lending to local councils…

corporate bonds, where you are lending to companies.

These other options are more commonly used by professional fund managers.

Individual investors often opt for bank or finance company deposits instead.

The term fixed interest generally refers to investments that pay regular interest over time.

While many have a fixed rate, others - such as inflation-linked bonds or floating rate notes - have interest rates that vary.

So it is a broad category including both fixed and variable structures.

It is important to note that the market value of fixed interest investments fluctuates with interest rates.

When interest rates rise, existing bonds tend to fall in value.

That is because investors can obtain higher yields from newly issued bonds.

Conversely, when interest rates fall, existing bonds tend to increase in value because they offer higher income than newly issued bonds.

Fixed interest is generally regarded as a defensive allocation.

It can help offset the higher volatility of growth investments such as shares.

Many investors base their allocation between defensive and growth assets on their risk profile.

For example, a typical balanced portfolio may be around:

40 percent defensive assets - cash and fixed interest

60 percent growth assets - property and shares.

For ethical investors, there is also the question of an ethical profile.

This might range from ethical light to ethical strong.

Today’s discussion focuses on an example that Money Matters would consider toward the ethical strong end of that spectrum.

The Fund: Sustainable Fixed Interest in Practice

In recent years I’ve been encouraged to see fund managers offering new sustainable fixed interest funds.

These provide ethical investors with more opportunities to aim to make money and make a difference through fixed interest investments.

Providing finance for sustainable projects is essential for achieving the United Nations Sustainable Development Goals.

These goals envision a world where all people can live productive and peaceful lives on a healthy planet.

Achieving that vision requires a transformation in how capital is allocated.

Money matters, and progress requires moving from business as usualtoward far higher levels of sustainability.

One relatively new fund available in New Zealand is the Trust Investments ESG International Bond Fund.

This fund provides diversified exposure to international fixed interest securities meeting certain ethical investment criteria.

Trust Investments is a specialist investment manager focused on ethical investing.

It has operated as a registered charity for over 24 years.

Last year Trust Investments moved from a passive approach to an active strategy with a significant focus on impact.

The Trust Investments fund invests in the Nuveen Global Sustainable Bond Fund.

Nuveen traces its heritage back more than 125 years, beginning in 1898 when John Nuveen founded his firm to finance public infrastructure projects.

Nuveen manages approximately 1.4 trillion US dollars in public and private assets globally.

Nuveen manages over 447 billion US dollars in fixed income assets.

Within this, more than 22 billion dollars are invested in ESG bonds, including over 10 billion in impact bonds.

The fund aims to allocate approximately 40 percent to impact bonds.

These are bonds designed to finance projects with clear social or environmental outcomes or both.

Examples include:

affordable housing

community development

renewable energy, and

protection of natural resources.

Nuveen has been recognised with many awards, including ‘Investment Team of the Year’ for the past three years in the Environmental Finance Impact Awards.

Introducing Jess

I'm joined today by Jessica Zarzycki, a co-portfolio manager for this fund.

Jess holds the Chartered Financial Analyst designation and has worked in the investment industry for 19 years.

Jess - welcome and thank you for joining us today. By way of a more personal introduction, what first sparked your interest in investing? Was there a particular moment or experience that drew you into the field?

First and foremost, thank you so much for having me here today.

It's wonderful to talk about what we do in impact and why. But it's going back a little bit further of how I got into this field.

It's been a journey. It wasn't this is what I want to do and where I want to be. There was an evolution in terms of how I got here. I've been investing now sustainably for just about a decade. But that path there took a number of different turns over the years. I would say, from a finance perspective, I had a strong interest in finance from a very early age, and I think that probably stemmed from my parents. They ran a small business. My mom did the books and the accounting. She was the one looking at the investments in the portfolio and trying to understand what she was doing from that perspective.

In a small business, you really start to see the flows of the economy, the good years, the bad years, and how she managed some of those upsides and downsides protected the portfolios - it was to me, looking back, pretty powerful to see what my mom was achieving at that point, for a small business, and trying to manage through those times.

I grew up in a small town - 2000 people - and today, I've been in New York City for 25 years - 8 million people. So quite a bit of a change on that journey. But it really rooted back to watching my mom and watching what my parents did from that small business perspective, and managing through some cycles in the economy.

What a wonderful example to have. What made you want to focus specifically on sustainable bonds?

In terms of my career path, I came to New York in 2003 - I'm going to date myself a little bit - I actually started working for a large bank through their private channels, and then moved over to the company I work for today at Nuveen, just over 17 years ago, in a research capacity. I worked in structured products for a minute. I then moved over to the International and Emerging Markets team, and that's really where I started to put the pieces together on the power of capital. And how you can start to drive capital in the marketplace to countries and individuals that really need that capital.

We're fortunate enough to have my boss, Steve Liberatore. He's been doing this for 30 years, and really combining that element of driving capital. So taking what I've done in the international and emerging market side and then really moving that into the sustainable side and the power of money to do good. It's pretty amazing.

Doing well and doing good has been my career business focus. It's really exciting to connect with people doing this globally, really at the forefront of the work. And when we think about investing from a sustainable impact point of view, most people think about investing in shares, because that's the most common type of strategies that are available. But you're investing in bonds. Can you explain in plain language, how can a bond create real world impact?

I will say I'm biased to the bond world and the power of bonds and really driving and scaling capital. What's different in the bond space versus the equity space is what we have today, are green, social and sustainable bonds. That allows us to direct capital to specific projects - for an issuer, a company, a government - that are going towards environmental and social outcomes. So, it's actually at the security level.

So we're able to drive and scale capital through the bonds and measure those outcomes. What we think about in the bond space is we're driving capital today for those issuers to meet some of those critical goals in the future. So if they have energy transition targets, if they're thinking about building out renewables in the bond market, we can provide capital today to have them reach some of those longer-term goals. And I think that really is the power of the bond market.

It's exciting. If we go back through your experience managing, specifically, sustainable bonds. Can you tell us more about that, and what have been some of the highlights and key points?

The sustainable bond market is issuing about US$1 trillion per year. So you can start again to see that scale around the sustainable bonds. That can really look like anything from a utility company that is looking for that energy transition to build out a solar farm to start to move away from fossil fuels. We can look at different sectors within the corporate bond market, where financials are lending to different types of issuers, again, thinking about renewable energy or providing capital towards green buildings, making those buildings more energy efficient.

I'm going to tie it back to fixed income, because everything we think about in the space is returns based and making sure that's at the forefront. But when you think about an energy efficient building, that often means that you have lower operating costs, which means you get more stable cash flows, and those are the buildings that tend to have higher tenant rates.

So it all flows together really nicely when we think about it in the bond space - about stable cash flows, driving returns. And then outside of that large scale corporate issuance, I think one of the other differences in the bond market is we also have access to governments, multi-development banks, and these are some of the key drivers in sustainability and driving capital to not just environmental outcomes, but social outcomes.

So we've seen a lot of governments get involved in the green, social or sustainable bond markets and thinking about how to deliver to the communities that they operate. Oftentimes this can be clean drinking water, clean sanitation - projects that are really important to the people. And when you get that right and people have access to electricity, access to food, access to clean water, it can change a life, and it also changes the economy. So always thinking about how these pieces work together to uplift an individual, but also uplift the economy.

Then at Nuveen, we're also pretty innovative in driving new structures to the marketplace. I'm going to lean into that; it also allows us to create opportunities within the strategies that we manage that are more diversified, less correlated with the broader markets. So thinking about increasing the population of the Black Rhino, Debt to Nature Swaps, which provide capital to areas in the Galapagos, which is some of the most diversified biodiversity and conservation areas that we need. There's a real power to some of these new innovative structures, which we tend to really drive, and help structure some of those deals.

Wonderful. It's exciting to hear from an investor perspective just how impactful money can be globally. You mentioned before your co-manager Steve and how you work together in this space. He's been involved for over 30 years. Tell us about how that partnership works between you. What sort of perspectives do you each bring to the investment process?

He's going to be mad, but I'll call him the Godfather of Green. He's been doing this for a long time, and he really has been the architect of our impact and ESG leadership framework. We created that framework back in 2007 using two key principles on impact: direct use of proceeds and measurable outcomes. He was also on the committee that wrote the green bond principles from ICMA. So he's been a real force in this space for a long time. Through the years, he's taught me a powerful message: we believe in this, and we're willing to be out in the marketplace and say when we think that the market's going in a direction that we don't believe in, and really backing why we don't believe in the direction of the market and holding true to the principles around sustainability that work for our clients and how we see the broader market developments.

We obviously have a fantastic relationship. He's wonderful to work with across the board. We complement each other in many respects. He started on the credit side and thinking about issuers on the investment grade corporate side. I came from the International and Emerging Market side. So marrying those pieces together and we both love markets, and we love to talk about markets. So bringing that together then driving the outcomes. It’s an amazing experience. I'm very lucky.

Nuveen as a Company - Purpose and Principles

At this stage, let's take a deeper dive into Nuveen as a company, to help us continue to set the scene.

Prospective investors often ask me how committed is this company, this fund manager, to the sustainability that the fund offers.

Talk’s cheap and lots of marketing folks talk about sustainability and being green or being socially responsible. I date my research in a formal sense with my PhD back into the 1990s, and came up with a framework of the Four Ps:

Purpose

Principles

Practices

Performance Measurement.

Let’s start with Nuveen’spurpose.

Sometimes purpose becomes clearer when you step back and look at the origins of an organisation.

In Nuveen’s case, the purpose really sits with its parent, TIAA — the Teachers Insurance and Annuity Association.

TIAA was founded in 1918 to provide retirement security for teachers and those working in education and public service.

TIAA states:

“Our mission is to serve those who serve others.”

Relatively few large asset managers have such a clear historical social purpose behind them.

That can be seen as one reason Nuveen is so active in impact and sustainability strategies.

Nuveen’s website refers to “Building tomorrow’s legacy” and notes that when John Nuveen underwrote his first bond in 1898, he had a vision that his new company could finance projects that help communities build for the future.

Nuveen describes its role as helping investors achieve their long-term financial goals while investing in ways that support communities and the planet. It states:

“We believe that every investment we make has the potential to expand into the lives and communities around us — a belief that guides everything we do.

Nuveen refers to its values as guiding principles that shape how the organisation works with clients and with each other.

Nuveen states that its core values — which can also be described as principles — help it deliver strong, sustainable returns, enhanced by employee and client satisfaction. So we've obviously got an employee before us who's very satisfied - four of those stated principles are:

Integrity

Collaboration

Innovation

Passion.

Jess, please elaborate on these for us and anything else you want to say about what it's like to work there, and what are those principles that guide you.

I look back at the mission of TIAA and Nuveen - it really resonates well with what we started out with - with my journey and how I got into finance and watching my mom think about her investments and what that looks like. So I will say every day I think about clients and making sure that we are doing the best for our clients and putting their money where it matters, and making sure that their returns are there. Then, when you can do it through a sustainability lens and say that you can have both, it's so powerful to me, and it just really resonates.

It's a nice combination with the journey of the historical clients of TIAA. When you think about teachers, university, health care, they've oftentimes been at the forefront of some of the journeys around responsible investments. They've given us feedback around what they're looking for and how we can drive some of this change. I think that's a really powerful, powerful message for me. I would say we do live those values.

When we think about integrity - just bringing it back to what I do, we think about integrity in terms of sustainability. What we're trying to do for our strategies and how we're trying to drive capital, making sure that we're not greenwashing in the space and trying to move the bar to a higher level. That's a very powerful element.

Innovation is an interesting one, right. The world is changing so fast and rapidly and trying to balance a fast-changing world and how much innovation, and then staying true to your core values around that integrity. For the innovation side from a sustainability perspective. we're looking at the new structures and driving change through the new structures. How do you crowd-in private capital into the space to deliver the enormous amount of capital that's needed around the world for looking at the UN SDGs (UN Sustainable Development Goals), and energy transition. I think innovation can be a really key principle in how we think about the sustainable sustainability space.

Crowding In

There are some interesting language things here. Sometimes when I go to the US, they ask me if I know how to speak English. And then when we add investment jargon on top of it, it can be a bit challenging. There was one term you used which I’d like you to expand on, for those listeners or viewers who aren't familiar with it - you talked about crowding in. Can you expand on that concept and what you're looking to do as leaders in this space?

The crowding in concept - probably something that you've been working on for 30 years - is how do you bring more capital into the market? How do you bring in private capital into areas and regions that have been more challenging or difficult to invest in? So potentially scaling up what government initiatives are through private capital - multi development banks that tend to be a larger player in the emerging markets.

How do you get some safety around what the multi development banks are so that private capital can come in and feel secure in their investments and really scale something that could be potentially US$100 million investment into several billion dollars. That's always the holy grail of this industry. There's a lot of push back at times on this space. So if we can do it in the right way, when we think about financial returns and we think about this market, it can be a really powerful tool.

One example that we've seen in terms of crowding in - or a different type of solution that came through the bond market - is we've invested in a multi development bank that supports immunisation in emerging markets. Initially, they were doing smaller scale segments of maybe US$10 million, US$15 million, to provide vaccines to emerging markets. In the bond structure, we were able to provide a significantly higher amount of capital. When you have a significantly higher amount of capital coming to the marketplace - US$150 or US$200 million - you're able to actually provide significantly more vaccines. When you think about being able to provide vaccines at a larger scale, at a faster pace, that actually means you're able to stem off some of the major diseases that are taking place in a society. And that's extremely powerful.

Again, I'm going to go back to the returns. It means that the economy is in a much better position when they're thinking about people that are able to be in the workforce, and you're not dealing with over capacities in hospitals. So there's real world experiences when you're able to deploy that capital and crowd in private investors.

Multi-development banks

So you're bringing other investors in with you. It's not just a Nuveen initiative, but because you're innovative, because you're making things happen, others can come in with you. You mentioned the term multi-development - can you expand on that in the banking context.

Multi-development banks, or super-nationals, the terms blend together. When we think about multi-development banks, we're thinking about institutions like the World Bank, the Asia Development Bank, the African Development Bank, where you tend to see large sovereigns be key shareholders in these development banks. Their goal and their purpose is to provide capital to certain regions or certain projects around the world to really uplift communities within those regions or support the private sector. Different multi-development banks - or super nationals - all have slightly different goals and objectives, but it's really that uplift of certain societies around the world.

Sovereigns

You mentioned the “sovereigns”, and again, just in a terminology context for a listener or viewer who's not familiar with the sovereigns that might be providing funding for these multi-development banks.

When you look at institutions like the World Bank that has entities under it, you'll see institutions - like the Inter American Development Bank, the International Finance Corporation - these all have different sovereigns or countries that are supporting this structure. Through that, you'll see the likes of the United States, the United Kingdom, Germany, and Japan as key stakeholders. They provide what we call paid-in capital - that’s capital supporting these institutions.

Oftentimes these institutions have what we call preferred creditor status, which means that they tend to be more senior in the capital structure, but they also lend at much more reasonable rates than what potentially the corporate or the borrowing country could come to the market for. So, there's definitely a little bit of concessionary lending coming from these types of institutions. But they get the benefit of that preferred creditor status.

When we use the term senior in a fixed interest or bond context we're talking about the lender having a higher ranking in the paying out of capital if things go wrong, or just eventually when payments are made.

So with all of that said, I'm now going to just briefly talk about Trust Investments because they're a key part of you being here and this strategy being available in New Zealand.

Trust Investments - Purpose and Principles

Trust Investments refers to having a mission:

“to generate investment performance for investors whilst delivering on environmental, social and governance objectives.”

And adds:

“We believe that companies with sustainable practices are better positioned for long-term success.”

I certainly relate to and agree with that.

Trust Investments describes its values as:

Care for the environment

It is important that we take care of the environment to help nature thrive and to maintain the delicate balance necessary to sustain life on this planet. This includes protecting natural resources and biodiversity, reducing air pollution and waste, and combating climate change.

Care for the community

Trust Investments says that everyone has a responsibility to do no harm, and to care for fellow tāngata — people — and for ourselves. Everyone deserves to have good health and wellbeing, as well as to live in an inclusive, safe, and sustainable community.

Care for equality

Society is founded on the idea of fairness and equality. Every person has the right to equal and fair treatment, independent of gender, race, age, religious belief, or sexual orientation. As a result, people feel socially connected and are able to participate in and contribute to their community, helping to create a safer, more prosperous, and more harmonious society.

Trust Investments states that it partners with renowned global asset managers and local specialists aligned with these values.

So from a Money Matters point of view, certainly commending that clarity of purpose and principles, mission and values. Jess, what's been your experience working with Trust Investments, and particularly drawing out these aspects.

The Trust Investment team is an absolutely fantastic team to work with. It’s really nice when you sit down in a meeting and you immediately see the alignment of principles, the integrity of how somebody thinks about the investment space and what they're trying to do. So while we went through a full due diligence process, both teams looking at the partnership, on day one, we saw the alignment between the teams on how we think about impact investment investing. About how we're thinking about environmental and social outcomes. So it was a perfect synergy for us. Hopefully, they feel the same way. It's been a wonderful partnership, and we look forward to working with them for many, many years.

Are there any other particular elements of what Trust Investments bring to this relationship that were particularly important for Nuveen, and can you tell us how the two roles work together?

The integrity and principles that come through Trust Investments was a key point that we anchored on - which aligns nicely with what we talked about earlier on the TIAA and Nuveen platform, and how we're thinking about this space. And thinking about, which is important to me but also important to the Nuveen team, is thinking about society. Making sure that the environment and society are working together, and how those goals may be used to support the community and support some of these broader goals.

I think Trust Investments continues to be at the forefront of that, and drive some of those changes. In terms of the partnership - they're here in New Zealand, I'm based in New York. So if there are any questions on different strategies and different opportunities, they are the key point of contact. We talk to them continuously over some of the opportunities in the market some of the challenges in the markets. They’re our New Zealand based partners and fantastic to work with.

Terrific and for viewers and listeners, it's quite a common practice that we've got a very large global player like yourselves partnering up with a local provider who can deal with all the legal elements and the marketing issues and the relationships locally. New Zealand's a pretty small place for a large group, particularly like Nuveen. And so for you to be here with us and for them to have made that possible, there's great appreciation of their role in the scheme of things.

Financials

If we now delve into the financials, you've highlighted this a few times as we discussed the context. But obviously, for investors, that fourth P of Performance Measurement has elements of finance and also elements of impact. We will come into the impact in a whole lot more depth shortly. But speaking of the financials, the fund information states:

“In accordance with the SIPO — the Statement of Investment Policy and Objectives — and the Trust Investments Ethical Investment Policy, the Fund takes certain ESG factors into account when making investment decisions.”

It continues:

“This is done to pursue certain responsible investing goals such as excluding companies involved in particular business practices.”

It also notes:

“This may cause the Fund to perform differently to similar funds that do not take ESG factors into account.”

And:

“There is also a risk the Funds may not achieve their responsible investment goals and so not deliver the intended outcomes for those investors who invested in the Funds for these reasons.”

Now that's quite technical and quite important in a podcast or in any investment context to have that disclaimer. With all of that noted, one question I often hear from prospective investors is whether it's possible to achieve strong financial outcomes while also contributing to positive change in the world. So, tell us about your view on that Jess.

You can have both. And that is something that we’ve believed in since we created our impact and ESG leadership framework, back in 2007. I think Steve was always the Godfather of Green, at the forefront around thinking about the space and our role in this space, in terms of the investment landscape, and thinking about those financial returns. So in 2007 it was, how do we provide clients, and potential clients, with the returns that they expect in different strategies based on different risk budgets, and how do we deliver impact? That has been at the forefront of what we do and why we do it, and what that fixed interest can offer in this space.

So yes, we absolutely believe that you can have both financial returns and impact. And we believe through the impact investments, that you can actually deliver alpha and mitigate risk within your portfolio. And that it's additive. Not something where you may have to be concessionary or give up returns. We think about it from the perspective that it's going to help drive some of those alpha components within the portfolio and help mitigate the risk within the portfolio.

Alpha

Terrific. And just again, for the jargon definitions that people might be wondering about, “alpha”. I understand what it is - as in seeking to outperform the market or adding value above just buying an index. Anything to add to the Alpha definition?

From the alpha perspective, we're looking to deliver returns above a potential benchmark, or return perspectives in the space. So when we think about the fixed interest markets, we tend to think about delivering income to our clients, which is important when you think about bonds being more of a safe haven asset. Then, how can you deliver returns above and beyond a benchmark? So for the impact space, we like to think about that you're getting additional financial information, which can help deliver alpha.

If I'm able to look at a large-scale utility project, in terms of a solar project, and see the megawatts per hour is being generated, and if it's not in line with what the company's expectations were, I'm actually able to potentially see that before other market participants. And if it doesn't make economic sense, then we may sell that particular security across the strategies, because we're able to see that there's a lower economic value in that particular particular project.

On the other side, we're able to potentially see if the project's going well - through the bond markets, we can actually lower their cost of capital in the space, provide lower cost funding for the corporation, so that they can actually build more wind and solar farms, crowding-in more capital into the space. If they're doing the right things, it makes economic sense.

Fixed interest markets tend to be the lowest cost of capital, and we can drive and scale capital for projects that make sense to help that company support their energy transition goals and generate alpha - because we've created more stable cash flows for that particular company, which is what we want to do in fixed interest and drive additional alpha. Which tends to for the right projects and more stable cash flows, you tend to see spreads compression, and that's exactly what we want to see in fixed interest is that spread compression because the company is doing the right things.

Spread Compression

Give us a definition of that for people who aren't familiar with it.

Within fixed interest, when you're looking at different issuers within the bond markets, there are ratings, which gives you a broad sense of the risk you are taking. So for a triple A issuer, which is the highest rating, they’ll have a lower spread. So it will be your local Treasury rate plus a spread above that local Treasury rate.

Let's say, in this market, a triple A issuer may have a spread of plus 50 basis points above your local Treasury. As you continue to go down that rating structure, spreads tend to widen out. So if you’re looking at a triple B issuer, maybe the spreads are plus 100 or plus 120 basis points. So, you need to be compensated for the risks that you're taking within the credit markets.

Our objective is to look at opportunities in the space where we think that there's mismatches, or where we think that they're stable cash flows, and we're going to earn a spread above treasuries. But it's a very stable company that we like that's a nice addition to different strategies that we manage. But that spread is telling you the risks that you're taking within that particular issue.

Going back to the roots of Nuveen and TIAA, we’re really a bottom-up fundamental credit shop. That means that we're doing a lot of work on the underlying fundamentals of the different securities that we hold within the different strategies that we manage.

We can contrast that with the top down, we've got a big macro economic view of the world, or crystal ball. We're guessing this and guessing that. In terms of the aspect of treasuries, and that's probably a more US term in the New Zealand context, people are probably familiar with government stock. And I used to teach financial management back in the 80s we talked about how that was the lowest risk of the fixed interest investments, even less risk, really, than the bank, because you've got the government with its ability to raise taxes and raise more money if it needed to. So can you just highlight why treasuries? And some people might say, “Oh, but look at the world, and it's a bit of a strange place. Are treasuries really that safe?” But just at the top of the pecking order in terms of the issuer that's able to issue at the relatively low cost of capital it's because they're relatively safe.

The Treasury market in most countries sets the tone for the market and tends to be the most liquid part of the markets across economies. The Treasury curve often times is viewed as more of a safe haven. There's a lot of dynamics that are at play today around fiscal concerns, and a number of different potential outcomes coming from some of the geopolitical disruptions and what that potentially means for longer term structural changes. But what we're broadly seeing in the market today is the markets functioning as you would expect.

Treasuries for global rates are the safe haven trades. You're seeing spreads start to move a little bit wider in these markets, as we're taking in different contexts around energy - whether this is a prolonged energy spike, or whether it's short term. The market's starting to re-price and try to figure out these moving pieces. But the treasuries are the anchor around the broader global markets. They play an important role, because they're also driven by Central Bank expectations, monetary policies and in the context of a global strategy, being able to look across different curves in different areas we have the ability to think about Central Bank reaction functions, to think about which societies and which economies are most impacted by prolonged energy rates, and be able to move to potentially countries or treasuries that may be less impacted by a prolonged energy spike.

That's the joy of active management versus passive - is we can move the strategies around to fit how we're thinking about some of these broader market developments.

Non-Concessionary

We talk about the concept of non-concessionary returns. I'll get you to explain what that means, and what evidence can we point to broadly about the ability for a strategy to achieve that non-concessionary return.

We’ve started to touch on this in earlier comments. When we think about construction, and how we think about this market, everything we look at is from a relative value perspective. We don't want to pay up for a green bond by an issuer that has a different risk profile.

So we want to be compensated for the risks that we're taking at that issuer level, even though we're directing capital into a specific project for that issuer. In our space, and how we think about this more broadly, there's not enough concessionary capital to drive the scale that we need. So we need a markets based solution to scale and crowd-in private investors.

So if you start giving up returns then you're always going to go back to the basics: Why am I underperforming? What's driving this underperformance? And if you say that we bought a bond that we didn't get compensated for, that doesn't do the market and the space any justice. So if you can deliver on those returns and deliver on those objectives, then it enables us to have more capital to do more in the longer term. So we don't believe, for our space, in fixed interest, that we should be the concessionary players. There's institutions like the World Bank, the multi development banks, whose role that is in this space. So we're driving in, crowding in capital, thinking about returns and delivering both returns and impact.

That’s going to be reassuring for many investors, because, of course, there is the need to make money and make a difference, and the ability to do both - the beauty of AND rather than the tyranny of OR is fundamental here.

So if we go back to this particular strategy, the fund information states that it “aims to generate a total return that exceeds the index — in this case, the Bloomberg Global Aggregate Index, one hundred percent hedged to New Zealand dollars”. Taking out the currency impacts is typical within the fixed interest space. That aim is over rolling three-year periods, before fees and expenses are taken into account.

To explain to our audience, when we talk about active management, the alternative is passive management, where a fund simply invests in an index and there are plenty of those. And in the ethical investment space, there are relatively light screens and then stronger screens in the passive space, but a purely passive investor isn't going to receive excess returns beyond the index performance, less the fees associated with that index fund. And of course, there are fees involved there. But conversely, we've got active investors who invest differently from the index with the aim of outperforming financially after fees and/or achieving more positive environmental and social impact. Now this can be a huge debate in the investment industry, passive, active and so on, so forth. Just broadly speaking, Jess tell us about your investment belief in active versus passive. You touched on it, but just to expand on that.

In terms of passive, you're taking the benchmark that you're investing in and looking at the returns that are coming from the benchmark. We believe active management is one of the best ways to address some of the capital through ESG, leadership and impact. Some of the most innovative structures and impact are not going to be benchmark eligible or fit into that index, passive-type structures, and those innovative structures are also where we can see opportunities in terms of generating alpha for the portfolio. The other piece is our ability to move around when there's dislocations in the markets, or changes in terms of economic growth outlooks, changes in terms of how we're thinking about credit spreads and moving the portfolio to better position ourselves for some of these macro changes in the marketplace. Active goes hand in hand with being able to adjust the portfolio effectively around some of these macro changes. Then, from the ESG and impact side, delivering on the impact through some of these structures that wouldn't be index eligible. That gives us an opportunity and a differentiation between what you’d see in the passive world.

Conventional Financial Practices

Before we dive even deeper into the ESG aspects, what are some of the conventional financial practices you apply when making investment decisions from a financial point of view?

We're looking around the globe for opportunities. That's a great thing when you think about global strategies. The world is my oyster for how we can invest and how we can think about this space. We're looking from a top-down perspective on some of the key changes in the macro environment. We're looking at monetary policies coming from Central Banks. We recently had the RBA (Reserve Bank of Australia) raise rates - they were the first mover on the upside, which actually had some global implications of people rethinking about where central banks are in terms of their cycle. We want to make sure we're incorporating some of those aspects into how we're positioned.

So you've got the macro and top down piece, but we're at Nuveen, and what we do well is bottom up - really thinking through asset allocations, like how we want to be positioned in certain sectors. We haven't touched on AI and some of the pieces that are coming through that. That’s a lens we're looking at in the marketplace. We're a little bit more conservative on some of those views.

We're looking at opportunities across different fixed interest asset classes. So what can we do in the credit space and the investment grade corporate space? Versus what do we see in asset backed securities, commercial mortgage backed securities, where we can stay very high in the credit structure, leaning into those triple A tranches, but getting a different spread profile than what we would get in investment grade corporate. Being able to use multiple levers in the space is important to us when we think about very broad indices for a global sustainable strategy.

Risk budgets

So the strategy that's being managed for Trust Investments is taking account of the benchmark and not wanting to be too far off that. And that's a challenge for many ethical investment firms, including the pioneers in the space, because people are wanting to ensure that they're not having to report to their investors and say, “Oh, we were very different on the downside to the market at this particular time”, because that will have people concerned. Of course, if they're very strongly above it, most people are not going to be particularly concerned. So we have this notion of differences compared with the market and in the investment jargon, we talk about risk budgets, and you've touched on that a bit earlier. So, can you just explain a little more about how all that works?

When we think about risk budgets, and how we invest is based on those risk budgets. It's a tolerance band of how much risk we can take versus the benchmark. We have the ability to take different risks in different areas of the portfolio that would feed into that risk budget guidelines. Everything we look at in terms of the portfolio is through that risk budget lens.

The strategies that we manage tend to lean more into a core-like solution – so it is going to be on the lower end of those risk budgets. So you shouldn't be surprised when you wake up in the morning that you're so out of line with what's happening versus the benchmark, because it's more of a core strategy. So within that risk budget, we're looking at opportunities, but we want to provide core-like returns to global sustainable strategies.

I've been looking at some of the share market investments, and obviously, with a lot of issues globally, some of the managers are saying, “Oh, we'd like to exclude Company X, Y and Z, given what they're involved in, but if we do that, we're worried that we'll be different to the benchmark. And what will investors say?” You've got a lot of tools and resources to help with that, which is heartening.

ESG and Impact Investment Process

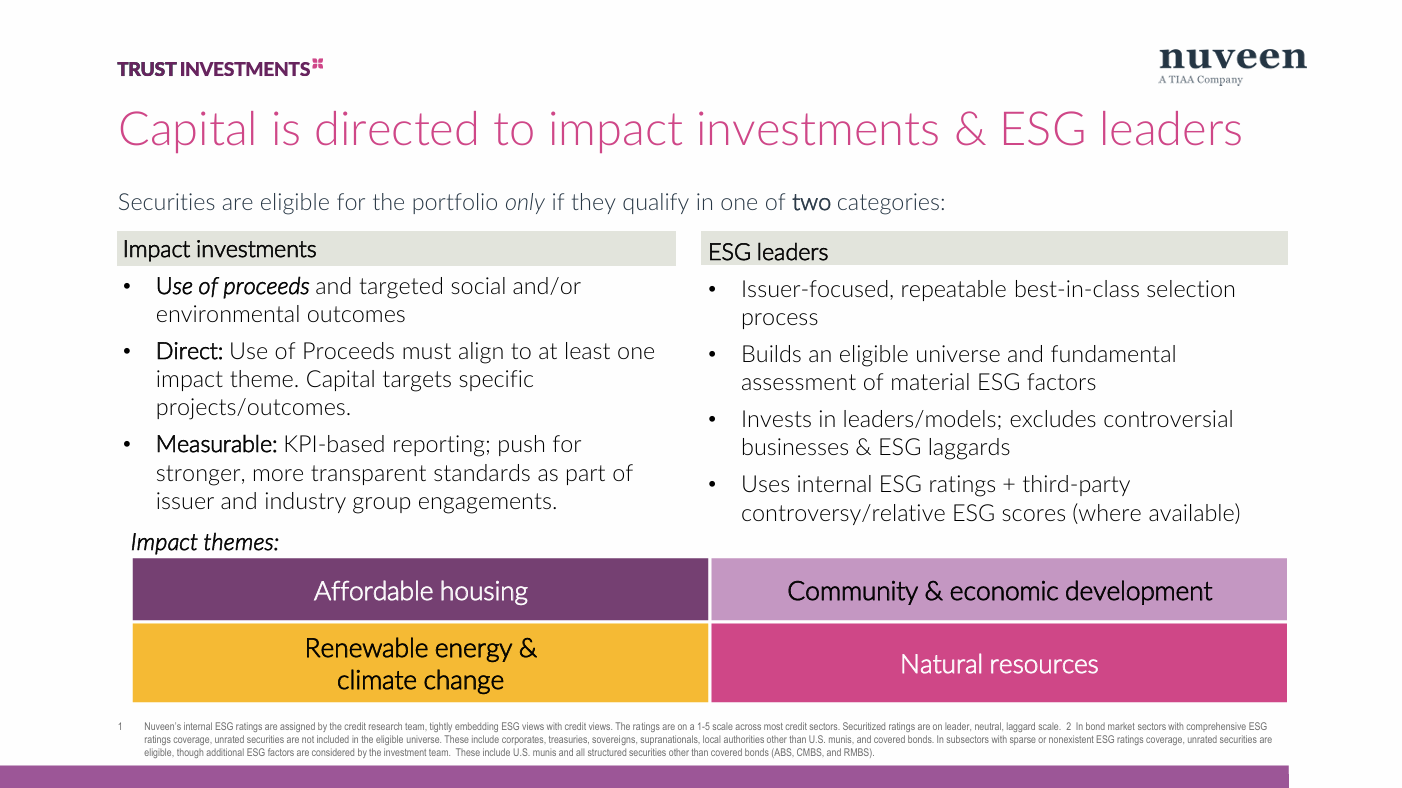

Let's now dive into ESG and impact in more depth. And in particular, we'll explore the difference between the standard ESG screened bond - Environmental, Social and Governance being the acronym, bonds issued by what Nuveen described as ESG leaders, and then what you're describing as impact bonds, and later, we'll look at detailed examples of how this process works in practice.

At Money Matters, when we analyse ethical investment funds, including fixed interest funds, we’re looking at three core ethical investment practices:

• Exclusions, also known as avoidance or negative screening

• Inclusions, also known as positive screening

• Engagement with companies to encourage change

Let’s begin with Exclusions. It's quite a significant Product Disclosure Statement, or PDS, that goes with these things, and obviously, anyone interested in exploring this further needs to study that and also look at the Statement of Investment Policies and Objectives, often referred to as the SIPO. It talks about things that are excluded from the strategy. Can you tell us a little more about the exclusions?

This is what you've traditionally seen in the marketplace. We've seen the evolution of the ESG and impact space, where exclusions were historically the primary driver of how do you not invest in something.

We've come a long way from exclusions, but they still remain important in the toolkit when we think about the sustainable space. They’ve coalesced around what you hear in the market, around weapons, tobacco, coal, nuclear, alcohol, gambling - those traditional exclusions. That’s where Nuveen is also sat in this framework.

The other piece of the framework is thinking about the leaders in the space, and we think that's an important component. Leadership is what allows us to continue to have a seat at the table; to have the engagements with issuers. If you're excluding money, the likelihood to have the engagement you need is less likely. But if you think about it from the ESG leadership standpoint, and you can do X, Y and Z to become an ESG leader, then I can have a more wholesome engagement.

There’s a broad market agreement around the types of exclusions that we've seen. But we tend to lean more into that ESG leadership and impact because it gives us a bit better seat at the table when we want to have those true engagements with issuers.

That's perfectly sensible. And let's focus in on the inclusions, because I think that's really a key point of differentiation. We're looking on the one hand at impact investments, on the other hand ESG leaders. We have a slide to illustrate showing this. Can you just talk us through the balance between those and how the two play different roles.

So since 2007 we've thought about this space through ESG leadership as one pillar of investments and then impact as the other key pillar of investments.

When we think about the ESG leadership component, it's really thinking about companies from a holistic E, S and G perspective that are leaders within their sector. They have strong governance, which is important when you think about credit fundamentals, to make sure management has strong governance practices. They're thinking about the social aspect, which can be from the safety of workers. Thinking about data privacy issues that can come through consumer products, how they're working on certain social issues related to that. And then what they're doing from the environmental side.

When you have a strong E,S and G framework in place, it means that the management tends to be more focused on their jobs and driving capital, or in driving investments and decisions around how the company runs a business, and not getting pulled away because they're in lawsuits around environmental or oil spills or safety issues with employees. When they're not being pulled away, they're doing more for the company and driving those changes.

So it's what the company is doing from an internal, holistic standpoint around this ESG framework. We think if we're doing it effectively, it should help mitigate risk within the strategies that we manage. It should be a risk mitigator, because you're thinking about companies that are thinking about their employees. They're thinking about environmental issues, and have strong governance.

On the impact side, it's really how can we drive capital for the goals of the company over the longer term, and provide this capital to these issuers?

If a utility company is looking at renewable projects, we're able to provide capital for them, for that solar or wind farm. So it's more of the capital providing to the issuer for specific projects, versus risk governance, risk metrics on the ESG leadership side.

This is not a static framework. As companies get stronger and get better, then potentially you'll see a new company emerge in terms of the ESG leadership. And maybe a company that has not been as proactive or has not done as good of a job, they may fall out of the potential eligible universe that we can manage through.

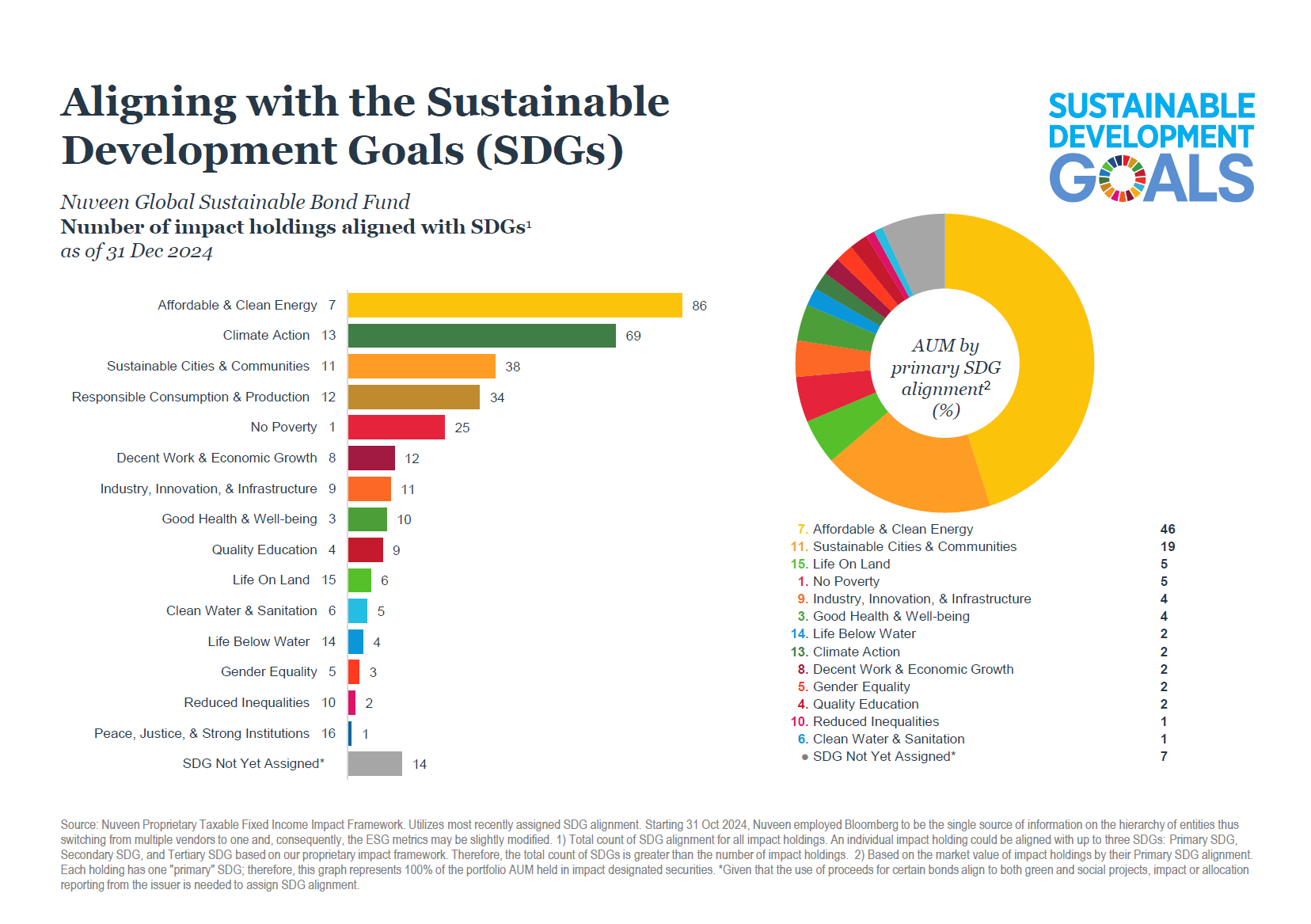

As we explore some examples of the fund’s impact investments, reference is made to the SDGs the Sustainable Development Goals. These goals were created by the United Nations in 2012.

They consist of 17 interlinked objectives designed to serve as a shared global blueprint for peace and prosperity for people and the planet.

The goals recognise that ending poverty and other forms of deprivation must go hand-in-hand with strategies that:

● improve health and education

● reduce inequality

● stimulate economic growth

● and address climate change while protecting oceans and forests.

Governments, civil society, and the private sector are all expected to contribute to achieving these goals.

As we can see in this slide, Nuveen reports on how investments align with the Sustainable Development Goals.

We’ll return to performance measurement in the SDG context shortly, but for now could you explain:

● why Nuveen reports in this way relative to the SDGs, and

● how these results ought to be interpreted as at 31 December 2025?

Our framework predates the SDGs. We focus primarily on our four thematic areas. Two are societal: affordable housing, and community and economic development; and two are environmental: renewable energy and climate change, and natural resources.

In 2007, we intentionally left these categories relatively broad so that the team could do their homework, and do the pre-engagement to understand exactly what we were investing in, and understand those measurable outcomes. So when the SDGs came into play in 2012, it's not a surprise that our clients were asking about them. So while we don't target or invest to the SDGs, what we have found when we do our homework and we find the right impact securities to invest in, that they aligned really nicely with what the SDG goals are.

To date, I think we've invested in, I'll say every SDG. The one that probably doesn't show up is the one where you support all SDGs. But we've done a number of projects in terms of life on land, life below water, thinking about gender equality, and ways to invest in affordable housing. We've seen a really nice diversification of underlying projects that have helped us to align with some of these SDG goals and objectives

It can be a challenge for the reporting by fund managers about what classifications apply for the respective SDGs. And looking at this particular slide, the question might pop up as to, why Zero Hunger, which seems a pretty fundamental SDG. In fact, it's SDG two.

In this case, we've got a slide which I took from the website, which talked about the bond investing in sustainably produced cocoa and wheat, and the same investment also being linked to SDG six, clean water and sanitation, and SDG 11, sustainable cities and communities. So for people looking at this particular slide, how does that multi classification process work as to what fits where.

When an issuer comes with a labelled green, social or sustainable bond, if it's a large corporation, the issuance size tends to be US$500 million to US$1 billion that are going towards specific projects. So they're not always aligned to one specific project. They can have a portfolio of different projects that align with different opportunities that they're seeing for their corporation, and how they want to direct capital.

In this example, for this particular bond, it's a really interesting case study, because you are focusing on the supply chain. Your focusing on farmers that tend to be in low income or emerging markets, that oftentimes we've seen in the world, where human rights issues can be a key component. So we spend a lot of time engaging with this particular issuer around how they deal with human rights, and what that potentially looks like, how they're trying to address some of the supply chain issues. So it comes with an approach around living wages, which is critical. When you think about providing living wages to somebody, it means that it can also support their family more broadly. That's a very powerful tool.

Within this particular example, it focuses on retraining farmers, which can take some time when you have generational farmers in this space, and their whole goal is around deforestation, so they can have more land, and saying, “No, you can do more with less”, and trying to retrain these farmers around different agricultural practices - that can be hugely powerful but extremely scary for farmers.

So that living wage element plus that retraining go hand in hand. That's what we're looking for. You can do something from the environmental side that's extremely harmful to the social side. So we want to make sure that they're both working together in respective ways. That you're not favouring one at the true detriment of another. So we like this investment, and looked at it for possible investment across the different strategies that we manage.

It's been a very topical area in New Zealand because chocolate is something that often has a focus from a fair-trade perspective. We've had a visiting academic from Australia who's been talking at the university and going through his work around chocolate and supply chains and doing a scorecard and ranking the relative suppliers. So if anyone's interested and wants to learn more about that, you need to do a bit more of a deep dive. But it's really important work and great to see the investment perspective.

Now you've talked about the four themes and why they are particularly suited and the way they are framed.

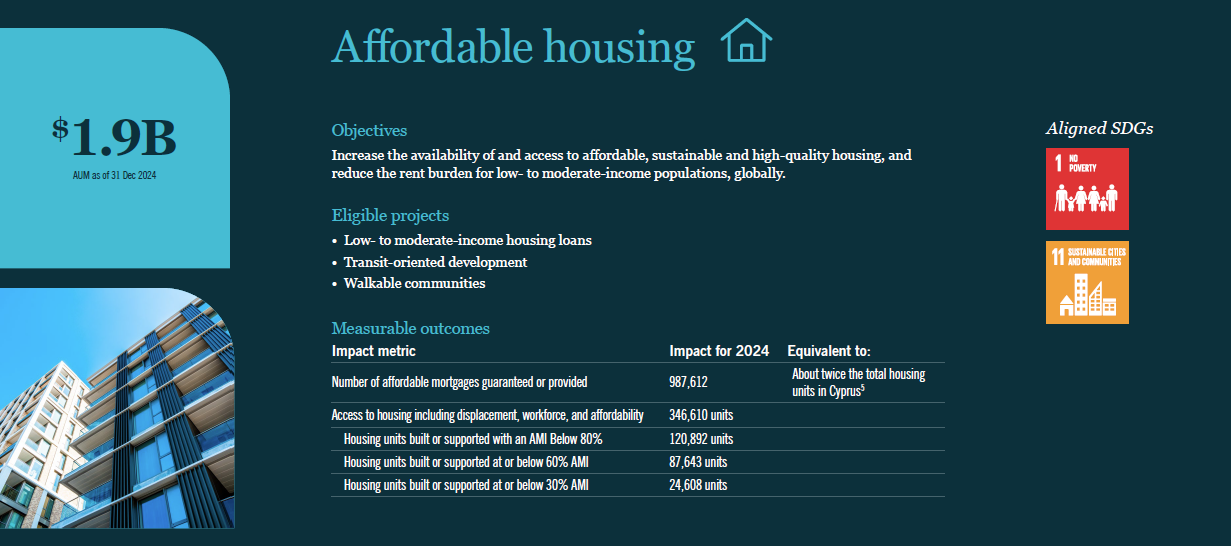

Theme 1 – Affordable Housing

Let's start with affordable housing and do a deeper dive there. In many countries, including New Zealand, housing affordability is a major social issue.

Using this slide from the Nuveen Global Fixed Income Impact Report, can you talk us through the types of bonds that support affordable housing and the extent to which these feature in the fund.

So affordable housing -we've been investing this way since 2007, thinking that this was a true social issue being able to provide housing to individuals around the world and having a safe place to stay can make a huge impact on an individual and on a family. So we've looked at affordable housing projects around the world, and different opportunities have presented themselves.

I'm going to use another term - development agencies - which tend to be focused on single country goals. We've invested in affordable housing opportunities in the Netherlands, in the US. In this example this was investing in affordable housing in India.

We were talking about risk budgets and how we're taking risk. We haven't gotten into structures that have a de-risking component or have backing from another institution that makes it a higher quality.

This particular example was guaranteed by US Aid, so it's backed by the US government, which is a very different risk profile than actually investing in direct exposure to an India issuer - which has a different risk profile than potentially we would be looking for, or making sure that we were getting paid for that risk. But we were able to provide that capital to the US Aid. From there, we were able to get the measurable outcomes on the affordable housing units built, which gives us, from a financial perspective, a bit more understanding of how that process works in India.

If we ever want to go down that capital structure, we have a baseline of what it looks like to invest in India – affordability, some of the issues and hurdles that even the US Aid company went through in terms of who they hired on the ground and what that looked like. This gives us a powerful way to provide capital to specific regions and countries in the world, maybe without taking the full risk of that of that region or that country.

Theme 2 – Community and Economic Development

Community and economic development is perhaps the broadest of the four themes. What types of activities does this encompass, and who are the typical issuers? Can you give an example of how a bond investment can support particularly underserved communities?

I would agree that community and economic development is broad, and it's served us quite well over the years allowing us to do the underlying work, to make sure we know exactly what we're investing and why. Coming out of COVID and during COVID, this came to the forefront of communities and investments in essential services - schools, thinking about walkable cities, public libraries - all these important features that are needed in a community.

So when we're investing in these types of transactions we're looking at how that’s going to impact the society which the projects are in. So we've seen a number of different opportunities in the community and economic development space. They tend to lean a little bit more into the development agencies and the multi development banks. Because when you think about the space in terms of return on investments, it tends to be a lower return on investment, so you tend to get more capital coming through the multi development banks and the development banks of a country.

But we've seen opportunities also through the financial sector that are lending to specific projects. We've also seen opportunities in blended finance through transactions like the Women’s Livelihood Bond, where we're investing in countries around the world, in emerging markets, and driving capital towards women, where there's a de-risking component within that structure.

So getting comfortable with investing in India, Indonesia, but not taking the full risks of some of those transactions.

The one on the screen is a Child and Youth Bond, so focusing on providing capital to some of the most important people on this planet and making sure that they're set up for success. Really driving change through how we provide health and services education. Oftentimes, that means putting a meal on the table and driving capital through transactions that are going to change a family's life. I think that's a powerful, powerful message.

And tying it all together, when we are going back to the multi development banks. We do get a spread above treasuries, but these are high quality issuers, and so it's a nice setup when we think about how we want to do portfolio construction and adding alpha and adding value without taking on significant risks.

Excellent, and people can see the slide, but also take a deeper dive on the website into these and the other case studies.

Another interesting aspect that you touched on briefly was this idea of what we call Orange Bonds. They are essentially, investments that take their name from the colour associated with Sustainable Development Goal 5, Gender Equality. The orange bond initiative was organised by the Singapore based impact investment exchange to support the development of gender focused impact securities.

The Orange Bond Initiative was organised by the Singapore-based Impact Investment Exchange (IIX) to support the development of gender-focused impact securities.

The Orange Bond Principles were published in October 2022.

Nuveen describes the purpose of these bonds as supporting gender-inclusive financing and mobilising capital to promote gender equality and women’s empowerment.

Jess, tell us more about this concept with an example from the fund.

The orange bond initiative came through a Singapore organisation called IIX. Full disclosure, I'm also on the Orange Steering Committee. Myself and Steve, we really believe in the power of this type of transaction Yhis organisation, and through the Orange Steering Committee, is really trying to push and drive change of delivering lending to some of the most underserved individuals around the world, maybe specifically in this transaction, focused more on the global South. But not just through the women's livelihood bond series, but really thinking about this as a concept for other issuers around the world.

The goal for the orange bond movement is to scale capital to US$10 billion by 2030. Sometimes in the financial markets, US$10 billion still feels like a lot to me. But when you think about trillions of dollars running through the systems on a daily basis - to certain people, it can seem quite strong. But this started with an US$8 million issuance. And we've seen the scale continue to grow through the women's livelihood bond series.

But we've also now started to see broader issuance coming through the orange label, and we've seen opportunities. I think the Japanese market has taken a hold of the orange label. Indonesia has done investments through the orange label. And we're hearing more opportunities potentially coming in Latin America. Now we're really starting to talk about scale and driving capital to an area that's been financially underserved for a very long time.

Thanks Jess - those are just fascinating examples and really heartening to hear about.

Theme 3 - Renewable Energy and Climate Change

Green bonds supporting renewable energy are perhaps the most widely recognised type of impact bond.

The energy transition is a major theme within the strategy. Talk us through the next two slides and how these investments contribute to climate and energy goals.

In terms of the green bonds, you're absolutely right. When we think about that US$1 trillion issuance in green, social and sustainable, we're still seeing about 70% coming through a green label, with renewable energy being one of the largest components of the green bond issuance. It's not surprising that renewable energy is at the top of the charts, because you're seeing large scale utility companies think about renewable energy, and that's an important component. We’re seeing scale coming through that space.

So we think from a scaling perspective, the green bond market is a great way to think about energy transition.

The slide on the screen is important to us, because oftentimes, when we're talking to different individuals around the world, they always point to private equity as the key pillar in terms of energy transition and technology. And private equity and equity has an important role to play. It has a very different risk profile than what we're looking at. But when we're talking about scaling, these two slides show the power of the debt markets.

On the slide you're looking at, in terms of equity investments in energy transition technologies, it's US$77 billion. When you're looking at debt and energy transition, you're looking at almost US$1.3 billion. That's the power of the space, and that's the power of scalability. And that's what we want to keep delivering. Because if we are going to meet these longer term, ambitious goals we need to be investing today. And the green bond market is a great way to scale and invest in these projects.

Just quickly, on the second slide, it gives a little bit of a historical perspective, and really continues to show the debt market playing a key role over the last three years in terms of this overall issuance. We expect that to continue, and we think that that's an important part of this puzzle.

Thanks Jess. Let's now go to:

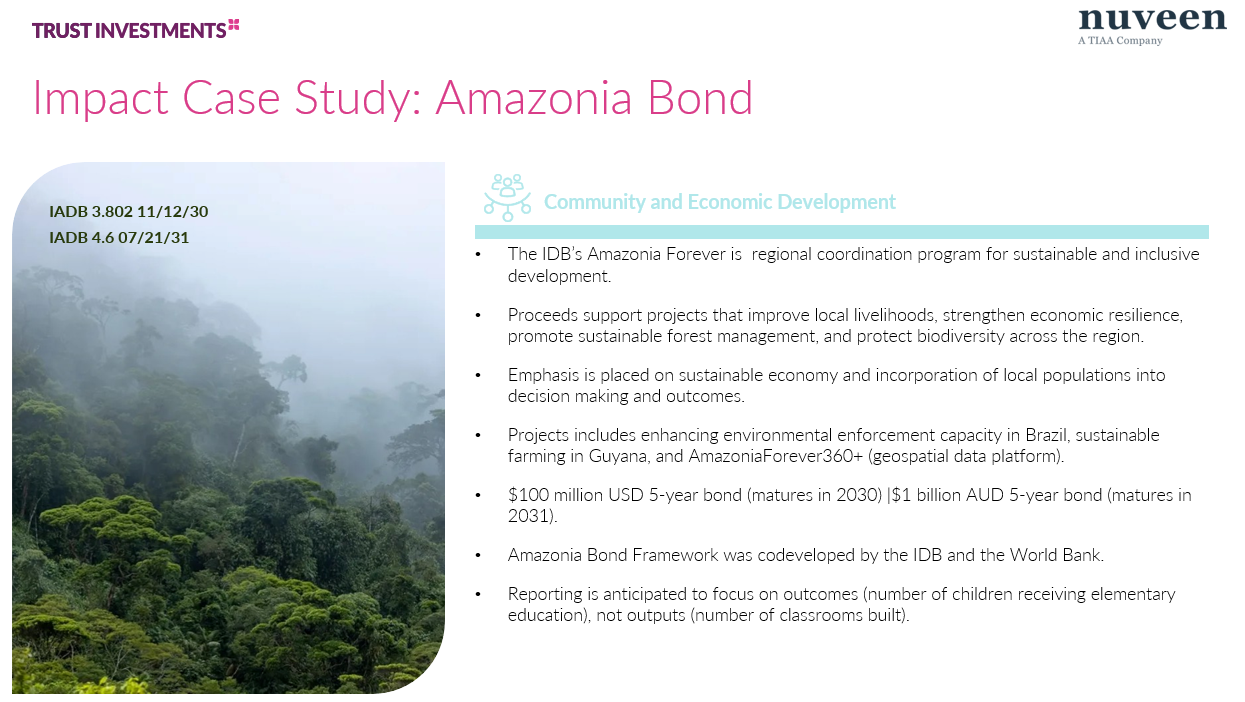

Theme 4 - Natural Resources and Biodiversity

Natural resources and biodiversity bonds are newer and perhaps less widely understood. We’ve got a slide about an impact case study The Amazonia Bond – tell us more about this one.

We've been thinking about natural resources and biodiversity and conservation for a long time, and we thought this was going to be a critical component of how we think about the world. Natural resources aren't indefinite. There's always concerns about water around the world, and there's a lot of different areas associated with natural resources.

What we've seen over the years - and this is going back to why we created a broad framework to be able to look at new and innovative structures - we didn't need the market to tell us natural resources were important. And that we should now be looking at blue bonds versus other types of bonds. We were at the forefront of looking at the blue economy. We're looking at the forefront of looking at reforestation projects, and we think that that's important.

In this particular case this one also leads into the community and economic development. So you see a blending of green and social working together in the community. So while it's supporting the communities within the Amazon region, it's also supporting sustainable agriculture. It's supporting practices around stopping deforestation, retraining people -individuals within the community, to maybe focus on ecotourism versus other industries. And really uplifting that community, which allows you to protect and serve the natural resources around it. So having the social and green really reinforce each other, I believe are the best types of projects, because that's how you also uplift the economy.

That is very powerful. I’m impressed by the reporting that occurs with the Nuveen context. Going back to the Global Fixed Income Impact Insights report, there’s a story titled:

“Reflections from the forest: World Bank Amazon reforestation bond.”

It’s a wonderful story of the Associate Portfolio Manager Adam Guerino following a visit he made in May 2025 to the Mombak reforestation sites.

If anyone listening would like a copy of this report, feel free to email me. Jess, can you tell us more about thar initiative?

Adam had a wonderful trip to to the Amazon - he's a great member of our team, so I'll give a shout out to Adam. This is an example of what we would call an outcome bond. The World Bank has been the pioneer of outcome bonds; they've issued a number of bonds now. We're seeing a decent pipeline through these outcome structures, which means that our returns are associated with the returns of the project. I'm going to get into this and what it looks like for this example on Mombak and the reforestation of native species within the Amazon, which is a little bit different than some of the other projects that we've seen.

Mombak is a company in Brazil, and they are purchasing or buying or joint venturing farmland around the Para region in Brazil. They’ve tended to look at farms that are second or third generation farmers where there's not much farming going on because there's degradation of the land. Then working with the communities around either purchasing or JVing this land, then replanning what would be native species around this land.

So within the case study, you can actually see – and so we have a video on this as well - what a difference a year makes, and what a difference three years makes in terms of replanning and the growth of the Amazon. What's interesting about this structure and this project is - we are definitely always focused on financial returns - but in this structure, initially, we take a lower coupon, and the difference between the market rate and the lower coupon goes immediately into Mombak.

This is scaling capital for Mombak so that they're able to buy more farmland, or JV more farmland, plant faster, use satellite monitoring - all these great things that will make the project successful. Over the course of the life of this project carbon credits are created.

So now I'm learning about the carbon credit markets, which is fantastic when I think about the direction of the space. We're not taking the carbon credits. We're about financial returns. The carbon credits are sold to a very, very, very high quality issuer who has longer term goals, but is part of the tech world. They are the off taker at an agreed upon price.

So when these carbon credits are created, we start to get more money back into the bonds. And so as the project becomes more successful over the period we actually have upside and alpha generation for the strategies that we manage. So, AAA principal guarantee. But that coupon component is actually where we see the alpha generation over the medium term. This is a powerful structure that we believe can be replicated - not just in Brazil, but in places around Asia, Europe, Africa, and that's where you see the scaling and crowding in of capital.

Coupon

And again, for retail investors, just a quick definition of coupon.

Coupon is the rate at which we would lend money to an issuer. I would view that as income for a client or an investor. So you're receiving a coupon on either on a semi-annual or annual basis, and that's guaranteed generated income.

And then we're seeing upside in terms of the structure of the bond, and I talked in the earlier introduction about the capital value of a bond. So there's potential for income, but also capital appreciation if things go well according to some of those strategies.

So another example is the Ecuador Amazon Conservation Bond, that uses a concept called a “debt-for-nature swap”. Many people might not have heard of that before. Can you explain how it works and what it achieves?

Steve's actually on the committee, similar to the green bond committee when they wrote the principles back in 2012, finalising the framework around debt to nature swaps. So you can see we're actively involved in industry groups to help steer and drive the industry forward.

On the debt to nature swaps this is an interesting structure in the marketplace, and again, has a blended finance component to it so that de-risking. So we're not taking the risk of Ecuador, but there's some type of either principal guaranteed or insurance around the structure. The way the debt to nature swap market works is you buy back higher costs of debt. And then, through this blended finance structure that has a guarantee or an insurance from an institution like the Development Finance Corporation in the US, you're able to issue new bonds at a lower coupon.

That differential between the cost savings of the debt that was brought back and the new debt that's being offered goes into a conservation fund. That conservation fund is then used to build projects, or create projects, within a certain region, in this case, in Ecuador. Then looking at the projects around ecotourism, true conservation in certain regions where they can actually make a conservation effort - where mining and energy companies can't go in and find resources there.

It really upholds the project, because you're working with institutions like the Nature Conservancy. So we're getting access to the experts, which is so important to us to make sure that the projects are going to be successful, that they're engaging with the communities, and that we're really making an impact in terms of those conservation efforts. So this is an innovative structure in the marketplace that can free up capital for a country, create more sustainable debt - which is different than sustainable investing - but put the country on stronger footing, and then deliver on some of these environmental outcomes that are so important to the world.

Another innovative example is the Rhino Bond, a wildlife conservation impact bond.

The Nuveen Global Fixed Income Impact Report for 2025 notes that these conservation projects use bonds issued by the International Bank for Reconstruction and Development.

Can you explain how these bonds work, including the payment-for-results structure, where returns are linked to achieving conservation targets?

We do have a video online, and I love it so if you do have a chance you should look at the video. But this particular structure, focused on two African reserves. There was a grant maker who was continuously providing money to the reserves to support the population of the black rhino. This is where scaling in capital can be really effective for a project.

In the bond structure, it was how do you make a difference and provide more capital upfront so you can get the satellite monitoring, you can move the watering holes from the fence line into the property to stop poachers, you can train more rangers. All of these things that you can do faster - actually helps to increase the population of the black rhino. This particular bond, the way the structure works is there's a hurdle rate on the black rhino. So if we are successful in terms of increasing the population of the black rhino above the hurdle rate, then that grant organisation provides a success payment to the bondholders. If we're unsuccessful, then they get their money back and are able to invest in a different project.

If we’re successful - which we expect to be successful given how the capital has been deployed - what we're seeing in terms of the measurement coming from the black rhinos, we'll get that additional success payment for our clients for investing in what we would consider an extremely innovative project.

Fantastic. Nuveen is also an active investor in “blue finance” — investments designed to support sustainable ocean and water-related projects.

There is another excellent video on the Nuveen website that talks about Nuveen’s role as the anchor investor in the world’s first Blue Bond, the US$15 million Seychelles Blue Bond issued in 2018.

Nuveen helped define the structure and bring other investors into this pioneering transaction, designed to support sustainable fisheries in the Seychelles, whose economy depends heavily on ocean resources.

The impact has been described as “a win for local fishermen, the world’s oceans, and investors.”

The 2025 Impact Report also references marine conservation in the Galápagos.

Tell us more about blue bonds — including how they are structured and how investors can support ocean conservation and sustainable fisheries through fixed income markets.

We're excited about focusing on the blue economy. I would say we're more truest - when we when we define blue, we really think about it in marine conservation parameters and how we're directing capital. The market's taken a more of a broader role on blue and also including components around clean drinking water and clean sanitation that has historically sat in our green framework. We think of it more as a terrestrial component.

When we think about the blue economy and what needs to be done around conservation, this is a really powerful tool for scaling. In terms of the Seychelles, it was a journey. Thinking about this back in 2018 - all the different moving pieces. From concept to reality, it was almost 18 months of asking: What are we doing? Why are we doing it? Does it have the ability to turn from US$15 million, which is relatively a very small bond issuance size, to billions of dollars. And we believed it did. So that's why we're willing to spend so much time around some of these innovative structures. Because we don't believe it's a one and done; we believe that we're setting a framework and a template to be able to build and scale and have similar pieces of the puzzle fit together around different parts of the world, and bring this into play. That's really important to us when we look at some of these innovative structures.

On the Seychelles, you're talking about two of the most important components of the economy: tourism and fishing. If you can teach somebody to fish on a more sustainable basis - that's important for the medium term trajectory of that economy. Making sure that you're not over-fishing in one year, so that you're hurting the longer-term outcomes of potentially that economy.

So focusing on those two key areas, really supports what the Seychelles is trying to do in the overall economy in that space. Then thinking about 30% conservation for the Seychelles - that's a large piece of both land and water - and thinking about how that ecosystem plays into tourism and sustainability from the conservation aspects.